Introduction of differential VAT rate, more harm than good

Potential loses in income and long-term fiscal weakness that would result from the announced introduction of differential VAT rate would exceed by far the financial relief that could be felt by socially disadvantaged residential groups if pricing down food products took place.

Therefore, we find that a greater number of alternative measures realized through the expenditure section of the budget offers more direct and better directed form of social welfare with the same goal. Below, there is only a brief overview of the basic pros and cons.

Differential VAT rate (pro and con arguments):

Pros:

- Key motif for introducing differential VAT rate is to cause lowering of prices of basic foods, i.e. products that would be covered by this rate. In short, this means that if the VAT rate for a certain product is decreased from the current 17% to 7%, than it is expected that the price of that product is lowered by the proportionate 10 percent points. Therefore, this measure can be described as primarily social in character, in terms of making it easier for socially disadvantaged residential groups to obtain basic foods.

Cons:

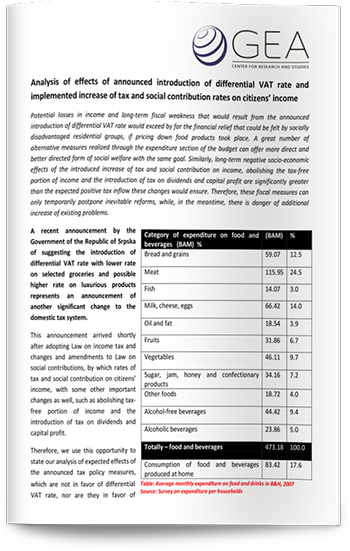

- This tax measure seriously threatens to the amount of income from VAT, bearing in mind that basic foods make high percentage of the entire consumer basket in the Republic of Srpska. For example, an average household spends around 55% of the entire food and drinks house budget on the purchase of bread, milk, cheese, eggs, meat and edible oil (study on households’ expenditure, 2007). Therefore, in order to compensate for such decrease in VAT income, it would be necessary to substantially increase the VAT rate on luxurious products, which will result in motivating tax payers to conceal sale of these products. For that reason, calculations related to introducing income neutrally VAT reform can be viewed as quite unreliable, because every tax system amendment affects the entire tax baseline.

- It is known that the decrease in tax rate often does not lead to proportional products’ price discount due to traders’ efforts to use part of this discount for increasing trading margin, which has proved as being very difficult to control in practice.

- All citizens consume basic foods so this measure will be felt by all, including the richest. Besides, analyses made so far show that a households’ monthly amount of money spent on food increases proportionally with income, so it is possible that this measure can actually bring relief in greater extent to rich households rather than to poor ones. On the other hand, social measures realized through the expenditure section of the budget offer possibility of much better directing of aid to those in need and less waste of funds.

Experiences from other countries show that after the differential VAT rate introduction strong political pressures emerge for supplementing the decreased VAT rate products’ list with additional products, which results in gradual extending of the list and further collapse of VAT income potential. The fact that many European countries introduced the differential VAT rate does not mean whatsoever that this is the best solution. It rather confirms the claim that it is very difficult to stop this process once differential VAT rates introduction is initialized.